Luxembourg

Luxembourg  Belgium

Belgium  Netherlands

Netherlands

AI agents are shaking the software industry and have triggered a historic correction across the markets. Is this a lasting threat or simply a sharp adjustment? Our expert analyses what really lies behind this technological shock.

A turbulent start to the year

Since the beginning of the year, investors have been questioning the outlook for software publishers as artificial intelligence — and especially agentic AI, capable of making decisions and carrying out entire tasks — gains ground.

In just a few sessions in early February, nearly $1 trillion in market capitalization evaporated from software and IT services stocks after Anthropic (a rival to OpenAI) unveiled new tools designed to automate legal and administrative work.

The sell-off was abrupt enough for some observers to describe it as a “wake‑up call” to the risk of AI agents bypassing existing applications altogether. Yet, when viewed through the lens of fundamentals, past waves of technological disruption, and the architecture of modern software, the picture becomes more nuanced: AI is set to reshape software — it plugs into it, but does not replace it.

AI agents unsettle the markets

The current turmoil began in February when Anthropic launched a new series of tools, including “Cowork”, capable of automating back‑office tasks in fields such as law, finance and administration. Markets reacted instantly: if an AI agent can read contracts, fill forms, trigger workflows and generate reports, why continue paying high prices for specialized legal, CRM or financial administration software? The most exposed companies fell first, before the correction broadened to the rest of the sector.

Some of the industry’s biggest names were hit hard. Thomson Reuters — heavily invested in legal software and services — has fallen around 37% since the start of the year. Salesforce, a key player in cloud‑based CRM, is down about 30%. Adobe, known for Acrobat, Photoshop and InDesign, has dropped roughly 26%, on top of a 60% decline from its 2024 highs. Overall, markets have penalised segments where AI is perceived as capable of automating “knowledge‑based” tasks: coding, analysing, writing, documenting or advising.

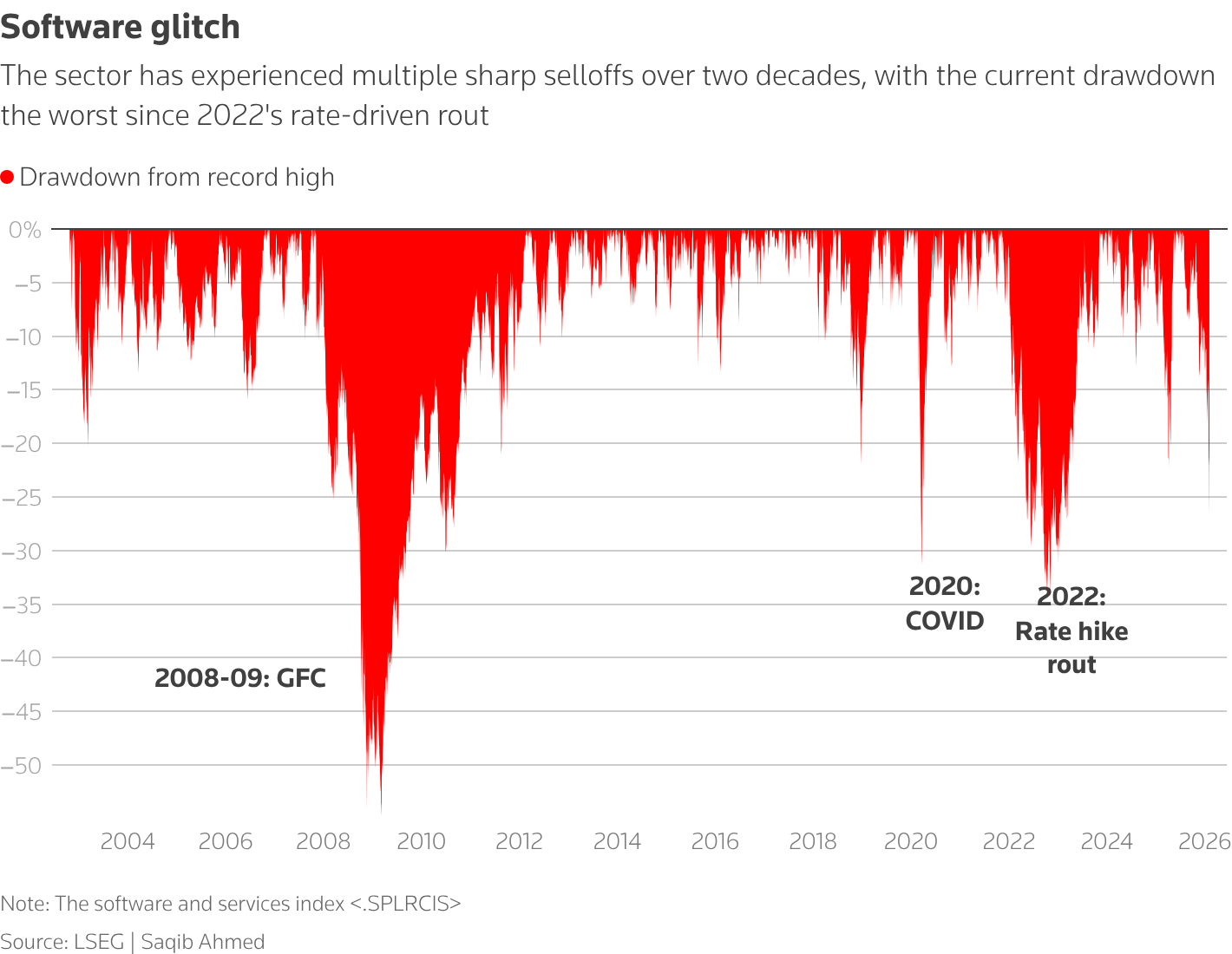

A chart from the London Stock Exchange Group (LSEG) highlights the scale of the shock: today’s drawdown already rivals major sell‑offs of the past twenty years — the 2008‑2009 financial crisis, the 2020 Covid crash, and the 2022 interest-rate‑driven correction.

Pressure similar to that faced by the press?

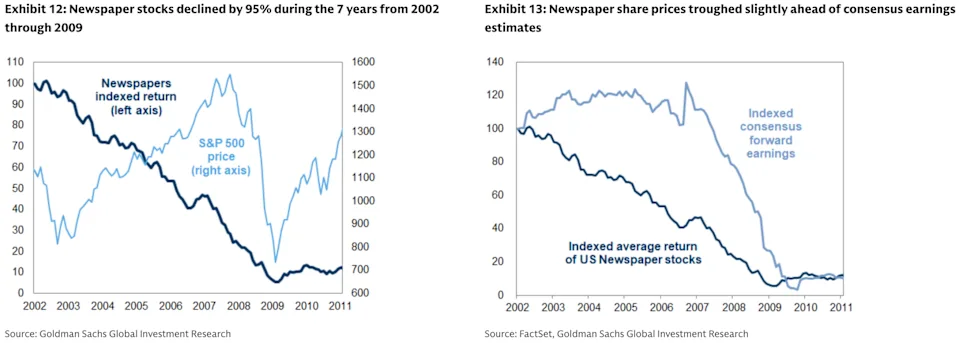

Goldman Sachs notes that U.S. newspaper stocks lost an average of 95% between 2002 and 2009, stabilising only once earnings forecasts hit bottom.

This comparison — frequently raised in market commentary — fuels the idea that software stocks may face long‑lasting pressure as AI progressively chips away at certain revenue streams.

The pattern is a familiar one: lofty valuations, a technology initially seen as a complement then re‑evaluated as a potential substitute, followed by a long reset period as competitive advantages erode.

For now, however, the parallel remains anecdotal: there is no visible cannibalisation of market share within the software industry.

AI agents: powerful features or software replacements?

Despite their sophistication, today’s AI agents are still best viewed as an add‑on to existing software ecosystems, rather than standalone replacements. Enterprise software is far more than an interface: it relies on structured data, access rights, compliance rules, audit trails and a web of integrations. AI agents must plug into these systems to access data, trigger actions and operate within predefined rules.

In practice, AI mainly changes how users interact with software: agents carry out certain tasks in the background, instead of a human user. But enterprise applications remain the central infrastructure for business data, controls, compliance and cross‑system exchanges.

Risks and opportunities for software vendors

The impact of AI will not be uniform. Some software segments — especially those offering highly standardised, single‑function solutions with limited proprietary data — are clearly exposed. In these cases, simple processes, accessible data and open interfaces make it easy for AI agents to replicate much of the functionality, reducing the need for multiple licences and lowering billable user volumes.

By contrast, vendors built on deep proprietary datasets, complex workflows and tightly integrated systems are more likely to use AI to reinforce their value proposition: more automation, more flexible pricing, broader usage without exploding costs, and a stronger platform position.

Research also shows that, for now, the deployment of AI agents remains concentrated in a handful of use cases — customer support, IT operations and administrative workflows. Scaling them requires not only technical investment, but also organisational and governance adjustments.

A significant but gradual transformation

The potential for transformation is substantial, but the transition will take time — giving established players room to adapt.

Early real‑world deployments show that AI agents most often integrate within existing platforms, particularly large ERP or CRM systems. They act as intelligent interfaces, navigating systems, launching workflows, consolidating data or making recommendations — without undermining the core role of software in data quality, traceability and compliance.

Against this backdrop, the sharp early‑year correction looks more like a rapid reset of expectations than an imminent shift to a “software‑free world”. AI is adding a new layer that redistributes value across the software ecosystem, rather than replacing these systems outright. For both vendors and investors, the key question is no longer whether AI will replace software, but how fast and how far the balance will shift between agents, AI infrastructure and enterprise applications.

Inform. Understand. Invest against the tide

Disclaimer : This is marketing communication. The themes and case studies above are based on CapitalatWork’s assumptions and are provided for illustration purposes only. They must not be used as a basis for making investment decisions. These assumptions do not constitute, under any circumstances, recommendations or advice relating to the purchase or sale of financial instruments or any other form of investment, nor should they be interpreted as such. CapitalatWork Foyer Group SA cannot be held liable if you decide to rely on our opinions or statements in general. This presentation does not contain sufficient information to make an investment decision. Recipients must ensure that they have obtained all relevant information before making any investment decision. Although the utmost care has been taken in preparing this document, CapitalatWork Foyer Group SA cannot guarantee that the information contained herein is up to date, accurate or complete, nor that it will remain so in the future. It is prohibited to distribute or reproduce this publication, in whole or in part, in any form whatsoever, without the written permission of CapitalatWork SA. CapitalatWork Foyer Group SA, as a licensed investment firm, is supervised by the CSSF (Commission de Surveillance du Secteur Financier – 283 route d’Arlon, L-1150 Luxembourg).