Luxembourg

Luxembourg  Belgium

Belgium  Netherlands

Netherlands

There are three major sources of performance in an investment strategy: asset allocation, active management, and security selection. Long-term results depend on the attention paid to all three drivers, rather than relying on a single lever.

At CapitalatWork, we are not merely bottom-up stock pickers. On several occasions, we have made high-level asset allocation decisions that proved meaningful—for example, highlighting as early as 2020–2021 the exceptionally expensive valuation of government bonds, or emphasizing, particularly since the Covid period, the role of equities and inflation-linked bonds as protection against inflation.

At the same time, we embrace genuinely active management across both equities and fixed income. This positioning is continuously adjusted through decisions on duration, currencies, credit exposure, regional allocation, and, of course, security selection. Everything is embedded within a clear investment framework in which top-down insights inform bottom-up decisions, and vice versa.

What has not changed

Markets evolve, but certain reference points remain constant. Credit spreads and equity risk premiums continue to serve as gauges of investor fear and enthusiasm, swinging like a pendulum. For companies, the decisive metric remains free cash flow—the ability to generate cash, rather than accounting earnings or EBITDA. Over the long term, a strong balance sheet and robust cash generation are the true determinants of resilience and survival.

Monetary and fiscal policy : setting the scene

Central banks primarily act as lenders of last resort, safeguarding confidence in an increasingly complex financial system. Recent episodes, such as the Covid shock and the rapid interventions to support certain banks, have demonstrated that their role extends well beyond simply raising or lowering interest rates.

Fiscal policy, meanwhile, has become structurally expansionary. The original Keynesian principle—accepting deficits during crises while generating surpluses during economic upswings—has largely been abandoned. Governments now face substantial and persistent spending commitments: pensions, healthcare, energy, infrastructure, and increasingly defense, with little political willingness to stabilize or reduce such expenditures. This contributes to an environment in which many prices—from supermarkets and local services to sports and leisure—appear increasingly disconnected from previous anchors.

Fixed income ; inflation and credit

Against this backdrop, our significant allocation to inflation-linked bonds remains both a macroeconomic and valuation-driven investment thesis. In our view, market-implied inflation expectations continue to underestimate realized inflation, creating a structural opportunity, particularly during periods when U.S. inflation temporarily rises above 4%.

In credit markets, spreads remain tight while corporate balance sheets are generally solid. We therefore focus on high-quality issuers and short maturities, aiming to combine attractive yields with prudent risk management.

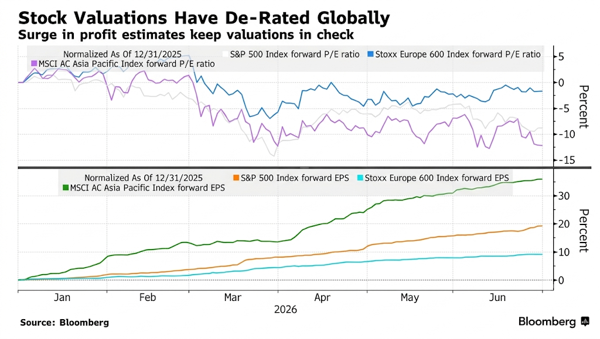

Equities : earnings growth, derating and hyperscalers

The fundamental engine behind the current bull market remains earnings growth, particularly the remarkable expansion witnessed in semiconductors and artificial intelligence. In recent quarters, this momentum has broadened to other sectors, enabling a form of derating: valuation multiples have normalized as earnings have caught up with what were previously considered stretched valuations.

This phenomenon has been particularly visible among the largest companies in the market. The weight of the “Top 10” stocks in the S&P 500 exceeded 40% before retreating toward 37%. Rather than passively following this concentration, we remain highly selective within this group. We favour companies where growth prospects, balance-sheet quality, and valuation appear aligned, while avoiding those where market enthusiasm seems excessive.

The year 2026 highlights an increasing divergence among these large-cap names, with the “Mag7” acronym masking very different business profiles. We are gradually building positions in companies where the growth-to-valuation trade-off appears most attractive, while remaining mindful of interest-rate sensitivity.

Beyond the “Mag7,” the concept of hyperscalers has become increasingly relevant. These platforms sit at the center of the cloud, data, and AI ecosystems, extending their influence across global markets. One critical observation, however, is that during this unprecedented investment cycle, the gap between accounting earnings and free cash flow has never been wider. This makes our free cash flow lens more essential than ever. It allows us to assess whether, once this phase of intensive capital expenditure subsides, these investments will translate into meaningful cash-flow generation—or whether they will remain largely a storytelling narrative fueled by excitement around AI.

AI : infrastructure versus storytelling

The key question is not simply whether AI represents a technological revolution, but to what extent it is already an economic revolution.

Signals coming from AI infrastructure suggest robust demand and therefore credible future cash flows. However, we remain more cautious regarding the monetization of large language models. Recent declines in certain token-spending indicators may suggest that converting usage into sustainable profitability could prove more challenging than expected for players such as OpenAI and Anthropic. Once again, free cash flow discipline remains, in our view, the indispensable filter.

Diversification and discipline

Balancing the desire to participate in exceptional growth stories with the need to maintain valuation discipline is a constant exercise. Too much reliance on storytelling can lead to unrealistic expectations, while excessive discipline can result in missing durable structural transformations.

Our answer remains simple in principle: true diversification across asset classes, sectors, geographies, and cash-flow profiles. In a world where certain assets—such as cryptocurrencies and gold—generate no free cash flow and can be subject to abrupt reversals, we continue to favour tangible and measurable drivers of long-term performance.